![]()

April 14, 2020

COVID-19 creates new opportunities for retail real estate investors and more attractive return profiles for the Marcus RE Fund I, LP

COVID-19 is accelerating the shake-out in retail real estate and pulls forward our thesis about opportunities in retail. The anticipated reshuffling of owners and tenants bring the risk-reward equation back into an attractive balance for investors once again.

Summary:

• Over-leveraged assets will be forced by lenders to recapitalize or sell, creating a favorable buying opportunity for class-A assets.

• Struggling retailers will fail faster, bringing about short-term vacancies. The reshuffling of tenants — from failing shopping centers, to successful ones — will require new capital for tenant improvements and create attractive entry points for equity.

• Uncertainty will shake out traditional owners who don’t understand real estate fundamentals well enough to “pick the winners.”

• Great rewards make the perceived risk “worth it.” Unlevered returns of 9.5%+ with 60% leverage and debt costs less than 4%, drive outsized equity returns. The risk-reward equation is “back in balance” in retail, making this category a legitimate option for most investors. Expect returns of 20%+ net of fees and carry, up from a 16% IRR, net of fees, pre-crisis.

Leverage, vintages, and incentives will drive deal volume. A robust economy has allowed over-levered landlords to hold on to their assets, but their time is up. According to the Mortgage Bankers Association, more than $163.2 billion of the $2.2 trillion (7%) of non-bank commercial loans come due in 2020, a 48% increase over 2019. CMBS loans account for $67.2 billion of those maturities. In 2021, those figures remain consistent, meaning more than 14% of non-bank commercial loans mature over the next 24 months. Those that are over-leveraged, or near the end of their debt term, will not have the incentive to infuse more cash into re-tenanting, thus preferring to sell, even if at a discount. With dividends suspended, institutional landlords and private equity vintages between 2010-2013, will be looking an opportunity to realign their portfolios, or exit altogether.

COVID-19 will shorten the timeline for failing concepts, centers, and retail formats. Cheap money in the recent past has allowed underperformers to hold on. COVID-19 creates a working capital requirement at a time when capital is more discerning of marginal businesses and assets. With risk-capital at a premium, the dying concepts will now be allowed to die.

Retail winners will co-locate and attract capital. Retailers will focus on their winners, and to the extent possible, co-locate with other winners. Nothing will kill a business faster than sitting next to empty space. Tenants, through recapitalizations via buyouts or bankruptcy, will use this opportunity to keep their well-performing locations. Other tenants will use this opportunity to relocate next to stronger performers, at more robust centers. In this way, Class A centers will consolidate successful tenants in the marketplace, making them more durable than they were pre-2008, not weaker. This reshuffling of tenants will require capital to take advantage of these “value-add” opportunities.

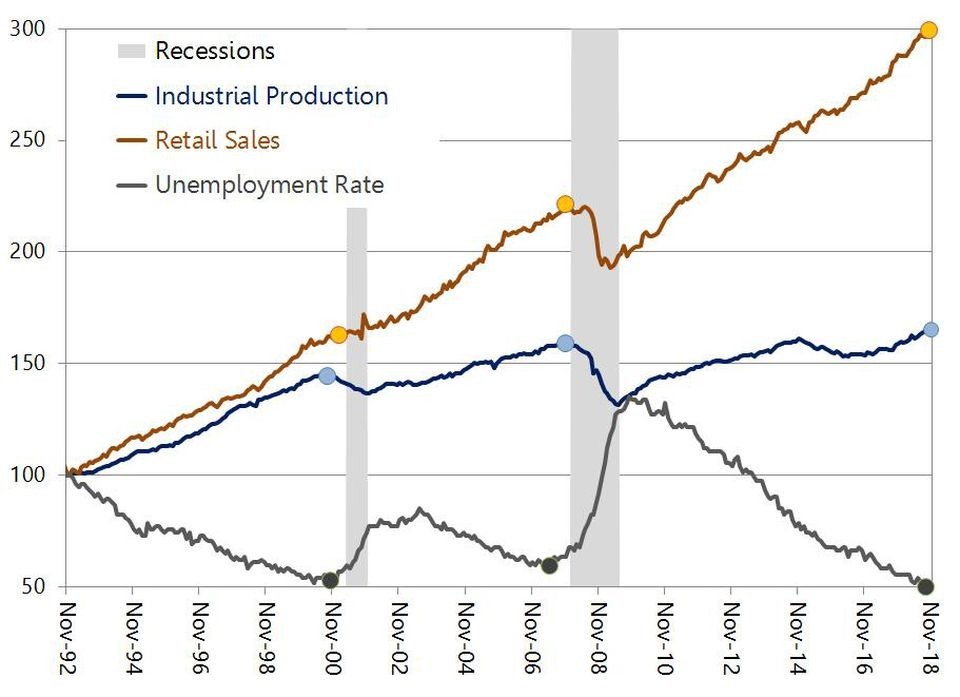

Figure 1: Federal Reserve of St Louis

The investment math works if you can avoid the pitfalls. Pre-COVID-19, patient buyers could purchase high-quality retail assets in the adjusted, high 8-cap rate level. Now, purchase prices should be in the mid 9’s or 10-cap range with debt costs less than 4%. With the math in place, the key to buying right, and driving 20%+ returns without undue risk, will be in understanding the real estate, the credits, the leases, and avoiding mistakes. A few final words:

• Do Not Fall Victim to Value Traps: Cheap does not always signal safe. Monitoring retailers’ credit, pre-pandemic revenue performances, traffic pattern shifts, lease provisions, market voids, and appropriate reserve levels all lend to confidence in post-pandemic risk-adjusted returns.

• Focus on Real Estate Fundamentals: No matter the economic climate, these fundamentals do not change. Retailers need access, visibility, synergy, and efficiency.

• Cash Flow is King: During uncertain times, cash allows assets to weather any storm. While appreciation can be great, current yields create certainty. Our returns are not created through financial engineering, nor via unrealistic terminal values.

Like any crisis, fear drives investor behavior. Today, an investment in retail investment opportunities shifts into a deep-value, highly opportunistic investment strategy for investors looking for high returns, current cashflows, and enduring hard assets. Those firms with ready capital, and the underwriting muscle to execute, will provide ‘certainty to close,’ putting the Marcus RE Fund I, LP at the front of the line in off-market transactions, and a seat at the table for any lender workouts that will be coming through the funnel.

Partnering with an owner-operator focused group that is skilled at actively managing assets through change will be critical to investment performance. Our thesis of high-yielding, stable, premier assets throughout the greater Midwest, with credit-worthy tenants, will thrive through the next cycle.

We look forward to partnering with you during these opportunistic times.

Regards,

Chris Nolte

President/CIO Marcus Investments

Please be advised that this letter contains forward-looking statements, estimates, and projections, and does not represent guarantees or assurances of outcomes in any manner.