SEPTEMBER 2019

Amanda Jogia +1 212-960-3316

info@primealpha.com 750 Lexington Avenue

www.primealpha.com New York, NY 10022

Bringing Alternative Investments 1

Insights from World Class Experts

RETAIL REAL ESTATE: AN UNDER-APPRECIATED ASSET CLASS

FOR HIGH CURRENT CASH FLOW YIELD AND PASSIVE INCOME OFFSETS

We recently published a report on shorting U.S. Malls back in July 2019. We have found that there are many ways that investors can invest in retail real estate by understanding the advantages of certain segments of Brick-and-Mortar and not overlooking those opportunities. The current market environment has created a unique opportunity to invest in retail real estate “power centers” providing investors with high current dividends while simultaneously creating passive income offsets.

Marcus Investments, a forward-thinking, dispassionate, third-generation Midwest family with a long history of investing in real estate and businesses focused on the customer experience, will walk us through a retail real estate opportunity in the greater Midwest.

THE CASE FOR BRICK-AND-MORTAR

The retail industry is beset by an existential crisis. Conventional wisdom holds that traditional retailers have stopped growing, as shoppers make more purchases online. Conventional wisdom, however, is often a poor substitute for true understanding. In fact, when one uncovers the facts about retail, one will find that much of this wisdom is false—or at best, only partially true—and that the industry presents opportunities for discerning and knowledgeable investors.

OMNI-CHANNEL RETAIL (RETAILERS WITH BOTH A PHYSICAL AND DIGITAL PRESENCE)

Consumers are not just purchasing in one channel but across all channels. The sales per customer increases as you add more channels versus staying the same, hence it is incorrect to assuming that 100% of the sales will move online when eliminating a retail channel. In fact, in Q2 of 2019, Target Stores (TGT) were praised by many research analysts for finally “cracking the code on delivering a seamless shipping experience between their physical stores and online – as many on the Street call ‘omni-channel shopping’.”

To begin, the retail industry is misunderstood. Retail sales across all channels, including brick-and-mortar stores, continues to grow with online sales receiving a disproportionate share of positive media attention although it represents only about 9% of total retail sales. In other words, approximately 91% of all retail sales still take place in brick-and-mortar locations. The data point most commonly referred to by those who would suggest that brick-and-mortar retail is on death’s door is online sales growth of 12.5% annually (2012-2016). This is an accurate statistic, however, 12.5% of the 9% of total sales results in about $40B in incremental online sales growth. In comparison, brick-and-mortar sales are growing at 1.3% resulting in $30B in incremental sales making brick-and-mortar retail still responsible for 43% of all incremental sales growth. (Deloitte Insights, The Great Retail Bifurcation, 2018)

IF RETAIL IS GROWING, THEN WHY DO WE KEEP READING HEADLINES ABOUT RETAILERS GOING OUT OF BUSINESS?

Consumer purchasing habits can provide some insight here. Consumer behavior is a unique reflection of their economic well-being. For 80% of consumers in the U.S., those with household incomes <$100k, the last 10 years have represented a dramatic worsening of their financial situation with little wage growth and an inability to participate materially in the rise of equity and real estate markets. In addition, this cohort of consumers have seen nondiscretionary expenses skyrocket: heath care +62%, education +41%, food +17% and housing +12%. Meanwhile, the other 20% of households, with incomes >$100k, have seen their discretionary income increase. The income bifurcation described above is profoundly impacting consumers’ spending behaviors.

We have separated retailers into three basic categories. Price-based and Premier retailers are dramatically outperforming so-called Balanced retailers who have been caught in the middle. These winners and losers have been produced by an industry undergoing a transformation, not a collapse. Today, more than ever before, retail real estate is not all created equal.

Price-Based: Kohl’s, TJ Maxx & Ross Dress for Less

Premier: ULTA, Costco, Pottery Barn

Balanced: JC Penny

NOT ALL REAL ESTATE IS CREATED EQUAL

Not all brick-and-mortar retail real estate is created equal. The real science is analyzing which real estate assets will see vacancy rates fall, occupancy rates rise and NOI (net operating income) eventually increase.

Investing in this contrarian asset class requires a bottom-up analysis of three factors:

1. Real Estate Fundamentals: High-quality real estate is essential when considering investment in a retail asset. Those assets that lack the qualities twenty-first century retailers demand from their brick-and-mortar locations will suffer. Elements that cannot be compromised include access, visibility, co-tenancy or overall design aesthetics.

2. Market: There will be successful retailers in the twenty-first century who have a significant brick and mortar presence. However, they will only make investments in markets where the demography is either stable or improving. Focusing on secondary markets requires an understanding of local consumer behavior, employer concentration and hyper-local growth trends.

3. Credit: Investing in retail real estate requires a sophisticated approach to managing risk. Performance of a retail tenant in a specific market could be fantastic but if the corporate entity is suffering there is significant risk inherited with the asset. Likewise, if a retail tenant has a strong balance sheet and healthy business fundamentals but is performing poorly in a specific market, there is more risk in the asset. A wholistic review of credit requires analysis of both the macro and local factors including: the retail company’s capital structure, the retail company’s fundamental performance, the local retail location’s health ratio (i.e. occupancy costs divided by revenue), the local retail location’s average weighted lease term and co-tenancy clauses that can be buried in local lease agreements.

After underwriting these three criteria, we can separate investment grade retail assets into four investment tiers:

• Tier 1: Trophy Assets: Trophy Assets: Fully leased, often urban, rarely for sale, levered cash flows of 4-5%, low vacancy risk, limited upside due to premium cost basis these assets command.

• Tier 2: SUTR (Stable Under the Radar) Assets: Fully leased or nominal vacancy, often suburban with strong real estate fundamentals, stable demographics, strong underlying retail performance, levered cash flow of 10-12%, vacancy risk varies based on credit profile of tenants, cost basis low enough to produce 15-17%+ IRR’s after assuming little to no NOI CAGR and significant reserves related to back-filling tenants that may vacate. In other words, the assets are priced well enough that they embody a significant margin of safety. The complexity of managing institutional grade retail assets combined with the headline risk of brick-and-mortar retail have turned investors off to most retail real estate. Sophisticated managers are finding these SUTR retail assets in secondary markets throughout the Midwest. The ability to discern between SUTR assets and those that will suffer to remain viable, as the retail evolution continues, is critical.

• Tier 3: Value Trap Assets: Varies from fully leased to partially vacant, appear to have the potential to be a Tier 2 asset but lack at least one of the three critical elements: strong real

estate fundamentals, stable or growing market, high quality credit profile. May produce immediate NOI but vacancy risks are substantially higher during macro-economic cycles.

• Tier 4: Value Add: Significant vacancy requiring major reinvestment. They either need to be repositioned from retail to another asset class, or require significant renovations to create, keep or increase NOI.

SUTR ASSETS: AN UNDER-APPRECIATED ASSET CLASS

These assets provide outsized risk-adjusted returns because conventional wisdom is that all brick-and-mortar retail is headed for extinction. They also require an experienced management team that can discern between SUTR assets and those that will suffer to remain viable as the retail evolution continues. Detailed, consistent and conservative underwriting standards, coupled with hyper-local market knowledge, allow us to see opportunity where others can only see risk. SUTR assets will continue to thrive in an evolving retail environment. It’s important to understand how co-tenancy impacts retailers’ performance and if you own the premier asset in any given market, not only will the asset persist, but rental rates will appreciate over time due to increased scarcity of quality retail locations.

Strong Real Estate Fundamentals

Fully Occupied

Investment Grade Tenant Credit

Low Cost Basis

SUTR Assets

“CLASS A CENTERS IN THE GREATER MIDWEST OFFER COMPELLING VALUE TO INVESTORS”

The retail real estate market has been under pressure for the past several years as e-commerce has been on the rise and several large national retailers have closed store locations due to the changing economic environment. Enclosed malls that were largely dependent upon the health of their department store anchors will continue to suffer increased vacancy. Lifestyle centers have had mixed success with the success of these assets largely depending on the execution of a mixed-use strategy.

Retail Power Centers with strong real estate fundamentals have been a bright spot in what has been a negative retail bias in the mainstream press. The middle-tier transaction segment, anywhere from $20MM to $50MM, has largely been ignored given its size is too small for large institutions and too large for country club real estate deals. Additionally, these retail power centers are being sold at elevated cap rates in the greater Midwest by owners who have an interest in redeploying capital at lower cap rates in the “SMILE” states (a region that includes the west coast, east coast and the southern edge of the country). An opportunity has therefore been created for discerning investors seeking high current yields and passive income offsets.

WHAT IS A RETAIL POWER CENTER?

Retail Power Centers are large, multi-tenant, open-air, retail developments with a mid-box lineup of retailers (e.g. Best Buy, TJ Maxx, ULTA, etc..) often accompanied by small shops, a shadow anchor big box retailer and outparcel users. Aggregate square footage tends to be no less than 100,000 square feet with quality retail power centers producing 75% or more of their NOI from tenants with “national” or “regional” credit, most of which are investment grade. Assets can be either stabilized, meaning the tenant mix is diverse with little to no term (lease) risk, or value-add which require redevelopment or re-tenanting.

SIZE OF THE RETAIL REAL ESTATE MARKET

It has been widely publicized over the past 15+ years that the United States is “over-retailed”, or in other words there is more gross leasable area (GLA) than there are viable tenants to lease it. A meaningful amount of GLA is now vacant with most of it functionally obsolete and more is to follow in 2019 into 2020. Quality retail real estate is becoming scarce. The growth of Amazon and e-commerce will not result in the demand for retail GLA to go to zero. However, quality real estate assets in stable markets that have capital structures capable of supporting low occupancy costs for tenants will remain in demand.

Potential investors in this asset class face significant barriers to entry as relationships have become the key to unlocking valuable insights that can be costly if left undiscovered. Relationships with retailers can provide insight into the performance of units in specific locations. Relationships with real estate professionals can provide access to assets not on the market and were thought to not be for sale. Relationships with credit analysts can provide insight into the financial health of private companies allowing for the necessary credit underwriting. Sourcing of opportunities requires more than hard work (or luck); the asset class demands a sophisticated approach to management.

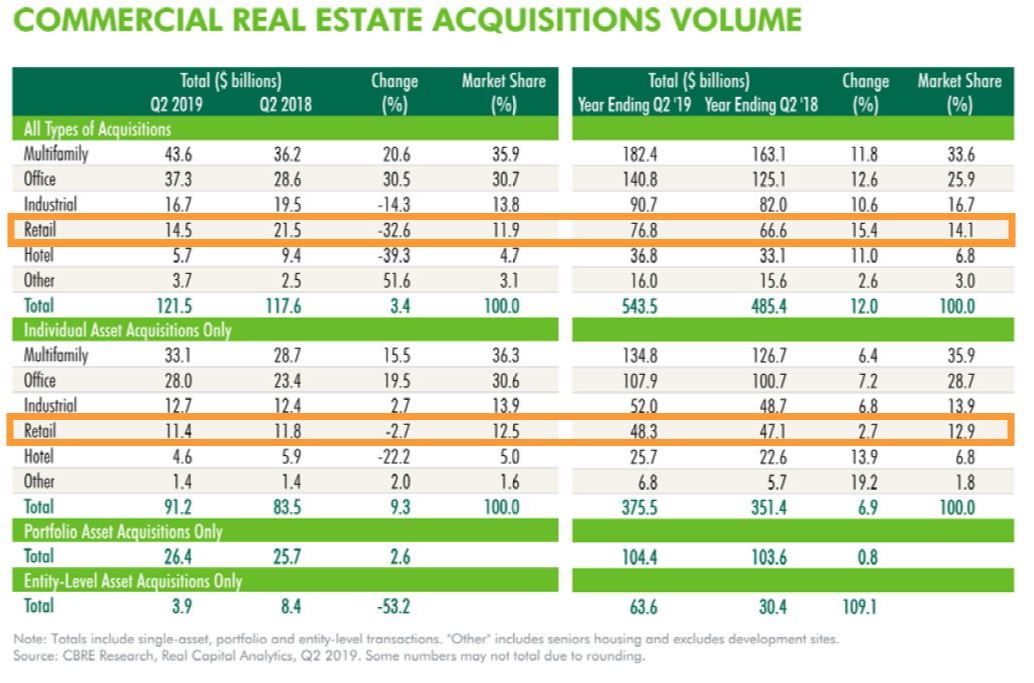

In the trailing twelve months (TTM) there were just under $77B of retail assets traded suggesting that the available market is significant. As managers deploy capital, they will find that sellers will be more willing to work with buyers who have a track record of closing and have the willingness to purchase portfolios of assets. The purchase of portfolios is often done with fund structures that desire large capital deployment into similar assets. Just under $29B of retail assets were traded as part of portfolios over the TTM.

WHY SHOULD AN INVESTOR INVEST IN RETAIL POWER CENTERS IN THE GREATER MIDWEST?

Retail Power Centers in the greater Midwest with strong real estate fundamentals, high occupancy and investment grade credit have been trading at elevated cap rates when compared with similar assets located on the east coast, west coast and in southern states. However, the existential risk facing retailers doesn’t change with geography. Purchase prices in the greater Midwest can be $120 to $170 per square foot, with replacement costs estimated to be well above $200 per square foot. Entering the assets at a low-cost basis results in outsized risk-adjusted returns for institutional grade assets generating gross project level yields of 18-20% with current yields, after reserving for tenant improvements and potential vacancies, at 10-12% annually. These high yields result in an investment that depends on the terminal value to produce less than 35% of the total investment return. This is a drastic departure from most real estate investment strategies today where investors are asked to bet on cap rate compression, NOI growth, or both to produce 70%+ of the forecast investment returns. While this approach is acceptable in certain asset classes, it does not provide the appropriate margin of safety that retail assets demand.

Investors seeking any of the following should explore investing in Retail Power Center assets:

• Significant annual cash flow available after reserves are held back to create the margin of safety

• Meaningful passive income tax offsets in year one of ownership

• Reduced correlation to interest rates given a focus on current cash flow and less reliance on terminal value to create returns

RISKS INVOLVED IN RETAIL REAL ESTATE INVESTING:

Illiquidity Risk: At times, real estate markets seize up and there are fewer bids even for Class A located real estate.

Mitigant: Line up debt maturities with lease term expirations as much as is practical. In addition, alternate exit plans are always being developed and refined. For example, many centers have “parts” that make up the “whole”. By identifying what parts can be sold and to which buyers, owners can selectively unwind a property and often with a greater return to investors.

Credit Risk: Poor or downgraded credits can put pressure on a retail power center. A poor credit mix can put the center at risk of vacancy if not managed properly.

Mitigant: A deep and fundamental understanding of the creditworthiness of each tenant is critical in making the initial purchase decision. Monitoring these credits monthly and creating a pipeline of A and B credits to fill vacancies is one way to create a sustainable retail power center.

Execution and Operational Risk: Management of large, multi-tenant, retail assets requires operational expertise in several areas of real estate including: negotiation of lease agreements with national retail tenants, design and construction of property improvements, property level accounting, common area maintenance allocation and reconciliation, property maintenance, negotiation and management of co-tenant restrictions, management of easement agreements and obtaining necessary approvals from local planning and building departments. Mismanagement of any operational components to the asset may result in lower financial returns.

Mitigant: This type of retail asset class is not suitable for purely financial sponsors. Risk is taken off the table when the sponsor of an investment is a hands-on operator who has in-house expertise in the areas of real estate noted above. With the Marcus family’s nearly 85 years of operating a variety of real estate intensive businesses, Marcus Investments approaches ownership of retail assets from the operator’s point of view providing a clear advantage when executing the investment strategy.

Macroeconomic Risk: E-commerce retail sales are growing at significantly higher rates than brick-and-mortar retail sales. Enclosed malls that are largely dependent upon the health of their department store anchors will continue to suffer increased vacancy. Lifestyle centers have had mixed success with the success of these assets largely depending on the execution of a mixed-use strategy. At the time of an economic recession, consumer discretionary income will go down and retail sales will slow.

Mitigant: Understanding the sales performance of retail tenants in specific locations can be very valuable as there should be an insistence on occupancy costs being less than 10-12% of gross sales. Where local store performance cannot be ascertained, technological solutions should be employed to better understand foot traffic at specific stores. While local store performance is analyzed, close attention must be paid to the retail tenant’s financial performance at a corporate level. Studying balance sheets, earnings reports and analyst reports is required today for successful management of a retail asset.

Figures for The Case for Brick-and-Mortar are from the Deloitte Insights, The Great Retail Bifurcation, 2018

Important Disclaimers

This article (the “Article”) is for informational purposes only and does not constitute an offer to sell or a solicitation of an offer to purchase any investment or any securities. This Article does not constitute investment advice and is not intended to be relied upon as the basis for an investment decision, and is not, and should not be assumed to be, complete. Readers should make their own investigations and evaluations of the information contained herein. The information contained herein does not take into account the particular investment objectives or financial circumstances of any specific person or entity who may receive it. Each reader should consult its own attorney, business adviser and tax adviser as to legal, business, tax and related matters concerning the information contained herein. Except where otherwise indicated herein, the information provided herein is based on matters as they exist as of the date of preparation and not as of any future date and will not be updated or otherwise revised to reflect information that subsequently becomes available, or circumstances existing or changes occurring after the date of preparation. Certain information contained in this Article constitutes “forward-looking statements,” which can be identified by the use of forward-looking terminology such as “may,” “will,” “should,” “expect,” “anticipate,” “target,” “project,” “estimate,” “intend,” “continue” or “believe,” or the negatives thereof or other variations thereon or comparable terminology. Due to various risks and uncertainties, actual events or results may differ materially from those reflected or contemplated in such forward-looking statements. Readers should not rely on these forward-looking statements. Certain information reflects subjective determinations which may prove to be incorrect. There can be no assurance that the estimates or projections will be accurate or that historical trends will continue. In considering the prior performance information contained herein, readers should bear in mind past performance is not necessarily indicative of future results. All rights reserved. The material may not be reproduced or distributed, in whole or in part, without the prior written permission of PrimeAlpha LLC.

Special Thanks to Our Contributor:

MARCUS INVESTMENTS | BERENGARIA

301 N Broadway, Suite 300

Milwaukee, WI 53202

P: 414.585.8870

Tim Anderson

Managing Director

D: (414) 585-8873

tima@marcusinvestments.com

Marcus RE Fund I, LP is a retail focused real estate fund managed by Marcus Investments, the family office of the Marcus Family. The fund focuses on “A” location open-air retail real estate power centers located in “B” tier or secondary locations throughout the greater Midwest generating high current yields and passive income offsets. The family is an experienced operator in the retail real estate market segment.

www.marcusinvestments.com

www.berengariadevelopment.com